Ways to Buy Municipal Bonds

- Buying Municipal Bonds

- Three Product Options

- Different Ways to Invest

- Important Considerations

- Other Things to Consider

- Investor Resources

Introduction

Millions of U.S. taxpayers purchase municipal bonds and invest in mutual funds and ETFs that own municipal bonds. Municipal bonds provide a way for investors to generate income while investing in infrastructure, such as roads, bridges, schools, as well as other needs in communities across America. Municipal bonds also may enable investors to earn money from their investment without paying taxes on the income.

Use This Guide to Learn About:

|

| Printable PDF Version of this Guide |

This information is for educational purposes only and provides a general overview of the subject matter and does not constitute investment, tax, business, legal or other advice.

Municipal Bond Investments

Many investment products, including municipal bond products, help investors achieve their financial goals. This section will help you learn about and compare some of your options.

Municipal Bonds

- States, cities, counties, territories and other governmental entities issue municipal bonds to raise money for public infrastructure and other capital, financing and cash flow needs. Investors buy bonds in exchange for the issuer’s promise to return the face value of the bond, called principal, plus interest. In essence, the investor is lending money to the bond issuer.

- Municipal bonds often are structured to provide tax advantages. If a municipal bond is tax-exempt, the interest income is not subject to taxation by the federal government and may not be subject to state and local taxation. Even if structured to be “taxable” under federal law, some state and local taxing authorities won’t tax the bond income. Certain municipal bonds, such as private activity bonds, are subject to federal alternative minimum tax (AMT), which means an investor’s interest income would be taxed at the applicable federal AMT rate if the investor was subject to AMT. Consult your tax professional to determine if any of these options are right for you.

- Investors should be comfortable not having access to their principal for the specified period until the bond matures (such as 1, 5, 10, 20 or 30 years) and with the frequency (typically semi-annually) of the interest payments. Investors receive their principal back when the bond matures unless the issuer is no longer able to pay. Learn about credit risk.

- There are two ways investors might receive all or some of their principal back early.

- The first way is through a bond call. If a bond is marked “callable,” then, with notice, the issuer may return all of the principal and pay interest only through the date it called the bond. Call provisions, including dates and prices, will be known at the time of purchase.

- The second way investors might receive their principal back early is through a bond sale.

- The amount of principal received at maturity may be different than the amount invested if an investor buys a bond at a premium or at a discount.

- If an investor sells a bond prior to maturity, the bond’s price may be more or less than the original purchase price of the bond based on changes in the interest-rate environment or credit worthiness of the issuer since the original purchase date.

- Investment minimums for municipal bonds are typically $5,000 per bond, so an investor with limited funds to invest and who is seeking exposure to a wide range of maturities, sectors and credits might consider a mutual fund or an ETF.

Mutual Funds

- A mutual fund is a professionally managed investment vehicle that pools money from many investors and invests it in a diversified portfolio of securities based on specific investment goals of the fund. Each share represents an ownership stake, or equity stake, in the fund. This gives the shareholder a proportional right, based on the number of shares owned, to income and capital gains (profit) or losses that the fund generates from the underlying investments.

- Similar to buying a municipal bond directly, there may be tax advantages for the dividends.

- Investors buy mutual fund shares, or ownership stakes, from the fund itself, through a broker or an investment adviser. The price that investors pay for the mutual fund is the fund’s per share net asset value (NAV), plus any fees charged at the time of purchase. Investors selling their mutual fund shares typically will receive the NAV at the close of trading on the day of the sale minus applicable fees.

- Mutual funds use differing investment strategies. Some invest in specific bond types such as ones issued by a particular state or with greater or fewer years until maturity. Others invest in riskier (often called “high yield”) or less risky (often called “conservative”) municipal bonds.

- Mutual funds offer investors more diversification than individual bonds.

- Shares in mutual funds do not have a coupon rate or maturity date.

- Minimum initial investments for mutual funds typically range from $500 to $5,000, although some fund companies do not require a minimum initial investment.

Exchange-Traded Funds

- ETFs are a bit like mutual funds and a bit like stocks. Like mutual funds, ETFs offer an investor an interest in a professionally managed, diversified portfolio of securities. Unlike mutual funds, investors purchase and sell ETF shares throughout the day at market prices.

- Similar to buying a municipal bond directly, there may be tax advantages for the dividends.

- An ETF’s market price typically will be more or less than the fund’s NAV per share. The ETF’s NAV is the value of the ETF’s assets minus its liabilities, as calculated by the ETF at the end of each business day. Changes in the value of the assets underlying the ETF and changes in investor demand for the ETF, among other influences, can make the market price go up and down throughout the trading day, sometimes significantly. An investor looking to buy or sell their share will receive the market price available at the time of purchase or sale, which could vary from the ETF’s NAV, especially during times of high volatility and market dislocation.

- Like mutual funds, ETFs use varying investment strategies. Depending on the fund, the municipal bonds it invests in may be issued by a particular state, have shorter or longer maturities, or have riskier or more conservative credit profiles.

- Shares in ETFs do not have a coupon rate or maturity date.

- Because they trade like stocks, ETFs do not require a minimum initial investment. You can buy an ETF for the price of just one share, usually referred to as the ETF’s “market price.”

Different Ways to Invest

A variety of investment services exist to help people invest in municipal bond products. Financial firms sometimes use different terminology than other firms to describe the same or similar services. Use this section to cut through the vocabulary and be able to identify and understand the type of service you’ll receive.

Brokerage Services

- When a brokerage firm is used, the assistance is transactional and time-specific. A typical financial professional at a brokerage firm accepts and carries out orders to buy and sell investments; on request, gives recommendations to buy, sell or hold a specific investment; and may agree to monitor investments in some accounts.

- These financial professionals charge transaction-based fees. Firms often charge a mark-up or mark-down for municipal bond trades, which are akin to the difference between the wholesale and retail prices for an item. The mark-up/mark-down is included in the price/yield of the bond, and the amount of the charge may be provided on their trade confirmation for certain trades. Firms may also impose a sales charge or fee for buying or selling a mutual fund or ETF.

- Brokerage firms offer three types of services: self-managed accounts (also known as self-directed accounts), financial professional-assisted accounts and managed accounts.

- Self-Directed Accounts: In self-managed accounts, you can buy and sell securities online without seeking recommendations or advice from an investment professional.

- Financial Professional-Assisted Accounts: In financial professional-assisted accounts, you can buy and sell securities based on the recommendations or advice of an investment professional. Transactions will only occur with the approval of the investor.

- Managed Accounts: In managed accounts, you give up discretion, and the financial professional can execute trades without consulting you, although they must adhere to the investment strategies specified for the account. See “separately managed accounts” below.

Investment Advisory Services

- Investment advisers typically charge investors a fee based on a percentage of the assets under management and there isn’t a separate charge for trades. The fee is agreed upon upfront. Generally, when hiring an adviser, investors decide whether they want to have a discretionary or non-discretionary account.

- Discretionary account: Investment advisers can act on your investment profile and their advice without asking you in advance of the trade.

- Non-discretionary account: The professional advises and then you decide what investments to buy and sell. The professional doesn’t have authority to trade without pre-approval. The assistance of investment advisers focuses more on investment portfolios or accounts, providing advice and monitoring investments over time.

Separately Managed Accounts

- SMAs are custom investment portfolios owned by an investor and managed by a professional money manager who has full discretion to execute trades. Like traditional investment advisory services, fees for SMAs are based on a percentage of the assets under management.

- With an SMA, your financial professional may rely on a separate portfolio manager (or multiple managers) to handle the day-to-day management of specific components of the portfolio. SMAs generally have specified investment criteria for the different asset classes they invest in. For example, for municipal bonds, the criteria may include certain maturities, coupons, credit risk levels and sectors, among others. SMAs typically much higher investment minimums than self-directed and financial professional-assisted accounts.

- Another term often used to refer to SMAs is wrap fee program. Though there are differences between these programs and other similar programs, they all involve the investor giving up discretion and paying an asset-based fee instead of a transaction cost. Going forward, we will use the umbrella term “managed accounts” to refer to these types of accounts.

Important Considerations

Use this section of the guide to better understand how various combinations of products and services (for example, the purchase or sale of municipal bonds through a brokerage account) can affect your involvement, investment strategy and wallet.

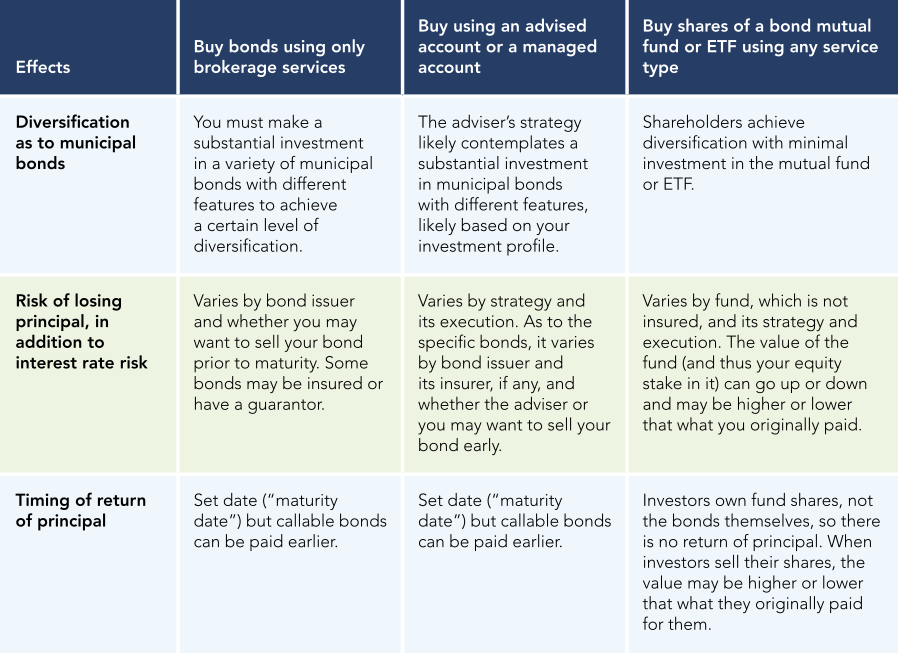

Who will be responsible for what?

- The investment approach you select affects how much work you have to do as an investor. Generally, investors assume more responsibility when they buy or sell municipal bonds through brokerage services than when they buy or sell municipal bonds or shares of bond funds through different means. Use the table below to better understand different responsibilities you would have if you were to invest certain ways.

How will this purchase affect my investment strategy?

- The investment approach you select may have implications for your broader investment strategy. For instance, if you hope to have access to your principal on a specified date, then it may be better to purchase a municipal bond than shares in a municipal bond fund. Use the table below to think through how the approach may affect your efforts to meet your financial goals.

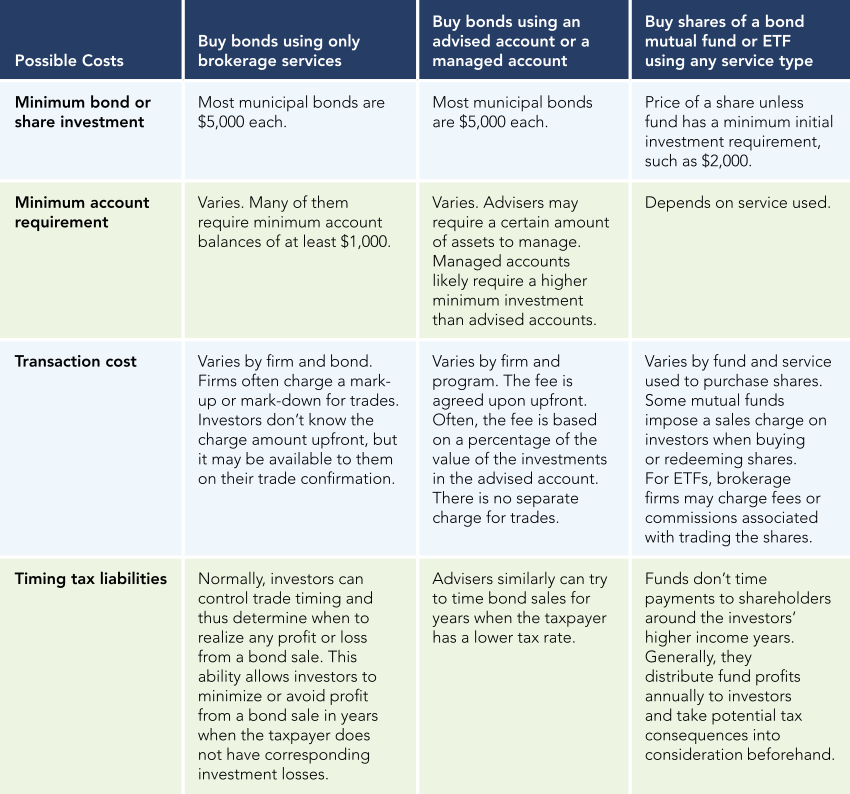

What will I pay?

- Last, there are different costs associated with different investment approaches. Review fund documents to understand types of fees and expenses that mutual funds and ETFs charge. You can access important fund documents using the SEC’s EDGAR system. Start here for help researching on EDGAR.

- Consider using FINRA’s Fund Analyzer. Enter “municipal” into the search tool. Click “View Fund Details” in any listing and then restrict the fund’s profile on the left side by clicking “Fees.” Upon viewing a few sample profiles, you’ll see that fund fees and expenses, as well as investment minimums, can vary, sometimes significantly.

Where can I find information about municipal bonds?

- MSRB's Electronic Municipal Market Access (EMMA®) website provides free public access to municipal securities data and market information, including real-time trade prices, official statements, credit ratings, ongoing disclosure documents, and yield curves, as well as several interactive tools to aid decision-making. EMMA supports municipal market transparency but is not a platform for buying or selling bonds. Explore the EMMA website.

Other Things to Consider

As you research different ways to invest in municipal bonds, keep in mind the following:

- Registration and qualification checks: Generally, the government requires brokers, investment advisers and their employers to be registered to conduct their business and to make certain information about their background and qualifications available. The U.S. Securities and Exchange Commission (SEC) maintains the Check Out Your Investment Professional tool so that the public can access this registration and qualification information for free. The Financial Industry Regulatory Authority (FINRA) offers a similar BrokerCheck tool. Similarly, the MSRB maintains a free list of brokerage firms that are registered to sell municipal bonds.

- Materials for investors: The financial services industry produces several materials for investors. It is important to read them thoroughly and carefully. Don’t hesitate to ask questions.

- Contracts: Investment professionals often address their duties and responsibilities to clients in their customer agreement or similar contract. Read the contract to avoid any confusion about the delineation of responsibility between the investment professional and you. For example, be sure you understand whether the investment professional has the authority to reinvest your principal and interest automatically into investments with comparable features to the ones you own.

- Disclosures: In addition to the contract, ask for and review any disclosures that may be relevant. For example, a managed account sponsored by an investment adviser must prepare a brochure about the program and provide it to investors before or at the time they enter a contract.

- Costs: Review all the contracts, disclosures and other materials about costs, fees and other expenses associated with investment services. Brokerage services tend to be a relatively less expensive option for people who don't trade frequently and have the time, skills and interest to research, select and monitor their investments. Note that using brokerage services to trade frequently can generate costs that are higher than the fee one would pay for investment advisory services or a wrap fee program.

Investor Resources

MSRB Resources

- EMMA website

- List of Registered Firms and Qualified Municipal Advisor Professionals

- Municipal Bond Basics

- How Are Municipal Bonds Priced?

- What to Expect from Investment Professionals

- Municipal Bond Investment Risks

SEC Resources

- Check Your Investment Professional

- Electronic Data Gathering, Analysis, and Retrieval (EDGAR) website

- Investor.gov

- Investor Bulletin: Investment Adviser Sponsored Wrap Free Programs

- Using EDGAR to Research Investments